{kind=link}

Today’s article comes to us courtesy of ACI shareholder Terry Moore, who recently attended the 2016 Economic Outlook Forum. During the event, Terry came to possess a number of interesting articles discussing many aspects of the world economy in the coming year. We present an excerpt of one of these articles for today’s Economic Earmark from a section entitled “Ending On A Higher Note”

The world economy will not celebrate major success in 2016, but a recession appears unlikely. Central banks will remain supportive with low interest rates and more QE if necessary. Major budget reductions will be delayed although financial markets will enforce at least moderate fiscal discipline.

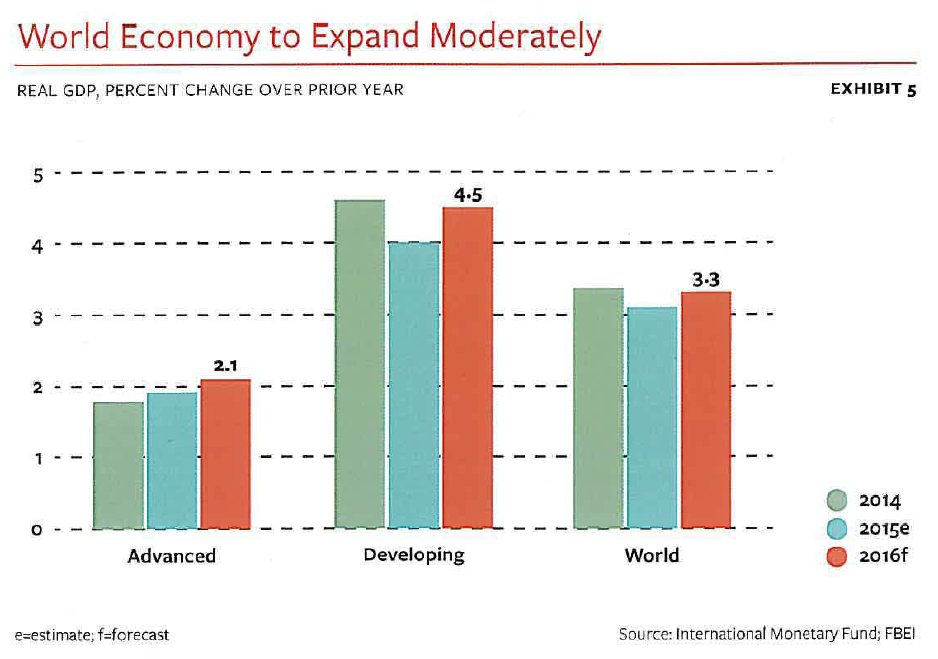

Look for global real GDP to expand 3.3% in 2016, up from the 3.1% pace of 2015. Advanced countries are forecast to see a real GDP gain of 2.1% as a group versus the 1.9% increase estimated for 2015. Developing countries are likely to see an improvement in their performance with a gain of 4.5% in 2016, following the 4.0% rise of the prior year. (See Exhibit 5.)

The Eurozone should be able to record a real GDP gain of 1.7% in 2016 compared with the 1.4% rise of 2015. The monetary easing by the European Central Bank (ECB) should help, giving support to such countries as Germany, France and Italy. Greece will likely see a second consecutive annual decline of more than 1.0% in real GDP as it struggles to adhere to the requirements of its latest rescue by the European Union, ECB, and International Monetary Fund (IMF).

The Eurozone should be able to record a real GDP gain of 1.7% in 2016 compared with the 1.4% rise of 2015. The monetary easing by the European Central Bank (ECB) should help, giving support to such countries as Germany, France and Italy. Greece will likely see a second consecutive annual decline of more than 1.0% in real GDP as it struggles to adhere to the requirements of its latest rescue by the European Union, ECB, and International Monetary Fund (IMF).

The U.K. is projected to see growth in the coming year close to the 2.5% it recorded in 2015. The Bank of England can be expected to join the U.S. in starting to raise interest rates. Canada will continue to adjust to a lower level of oil prices but should benefit from some strengthening in the U.S. economy. As a result, it should see real GDP growth of about 1.8% versus only about 1.0% in 2015. Finally, Japan will modestly boost prospects of the developed nations by posting a real GDP gain close to 1.5%, up from only around 0.7% in 2015. Prime Minister Abe will promote more stimulus, while exports should benefit from a lower value of the yen.

Although China is likely to see slightly lower growth in 2016, many other developing nations should see relief from stabilization in commodity prices by year-end, weaker currencies, and some firming in the economies of the major industrialized economies. Many countries in Asia, Eastern Europe, Africa, and Latin America should see improved prospects. Progress in terms of economic reform will help India achieve one of the fastest growth rates in the world, with an estimated rise in real GDP of around 7.5%.

Wide divergences in performance will characterize Latin America. Mexico should benefit from gains in the United States and the peso’s decline, but Brazil will shrink further as a result of poor economic policies. Government changes in Argentina and Venezuela could offer help to those beleaguered economies.

Depressed oil prices represent a primary negative for certain nations, while they benefit others such as India and Japan. Russia’s economy will continue to shrink, as it continues to suffer from the impact of lower energy prices and economic sanctions imposed because of its intervention in Ukraine. Countries in the Middle East heavily dependent on oil, such as Saudi Arabia, will see significant stress under the pressure of low oil prices and budget cuts in the face of climbing financial deficits.

On balance, growth conditions should improve modestly around the world in 2016, but the under performing outliers will be notably off-key.

Additional information about the Economic Outlook Forum can be found HERE.