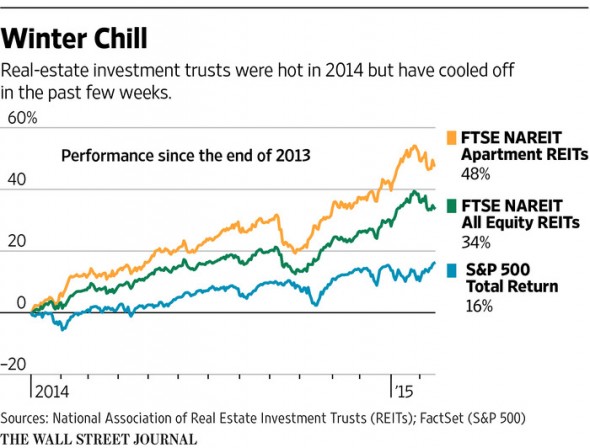

After a banner year in 2014, the party might be coming to an end for real-estate investment trusts that specialize in residential apartment buildings.

Last year, the category produced total returns, including dividends, of 39.7%, the best among all real-estate stocks, according to the National Association of Real Estate Investment Trusts. REITs overall recorded a total return of 28% last year, as the economy improved and interest rates stayed low.

But in the last month, investors and analysts have cooled to the sector. REIT total returns are a negative-1.7% so far in February, with apartments stocks returning a negative-1.1%. A handful of analysts have downgraded the apartment sector on fears it is overvalued and won’t generate the growth in revenue it posted last year.

“The problem is that the stocks are a bit more expensive, and you’re getting slower growth,” said Haendel St. Juste, a REIT analyst with Morgan Stanley. A year ago, Mr. St. Juste says, most REIT stocks were trading at a discount of between 10% and 15% of the value of their assets. After last year’s rally, most are now trading at a premium of 10% to 15%.

There is also talk of an oversupply of apartments in markets where there hasn’t been enough job growth to support demand. Washington, D.C., has seen a huge uptick in supply over the last three years, while in the Texas oil belt the falling price of oil has sparked fears that jobs will dry up.

Builders in the past six months have started construction on new multifamily apartments at an average pace of 357,000 units a year, 26% more than the 30-year average, according to Evercore ISI. The investment bank predicts negative demand, or a rise in vacancy rates, for apartments over the next year for Houston, Washington, Charlotte and Austin, Texas.

“Overbuilding concerns will remain a focal point for REIT investors over the next few years given the current pace of permit activity and new starts,” says Steve Sakwa, an Evercore REIT analyst.

Houston-based Camden Property Trust, for example, last month reported it had produced same-store revenue growth — a common gauge of REIT performance that measures how much income a company’s existing assets produce — of 4.5% in 2014. The company is forecasting the same measure will fall between 3.75% to 4.75% in 2015.

“If you look at Camden, we’re a serious example of a stock being beat up by Texas,” said Chief Executive Richard Campo. Camden’s share price hit $81 in late January, topping the company’s previous peak in 2006. Investors have since pulled back amid worries that Camden, which gets 13% of its net operating income from its properties in the Houston area, is too dependent on Texas.

In another Camden location, outside of Atlanta, Mr. Campo said there is likely some rental increase fatigue after a 9% rise in rents last year.

Mark McAllister, who manages the $1.1 billion Clearbridge Tactical Dividend Income Fund, of which up to 25% is invested in REITs, said he increased his allocations to apartment REITs including AvalonBay Communities Inc., Equity Residential and Aimco in 2014, but that he has stopped buying apartment REITs for the time being.

“You’ve got more supply coming into the market than people were hoping, and we’ve had earnings reports that on the whole I’m not thrilled with,” Mr. McAllister said. “I’m not feeling motivated at these valuations to sell right now. I’m sort of just standing pat now.”

Not all market-watchers are so gloomy. David Toti, who covers REITs for Cantor Fitzgerald, said that even if the sector’s income growth wanes, any growth is attractive in a low-interest-rate environment.

He added that landlords will benefit from a shift in American attitudes about living space: More young people prefer rental apartments to owning a home, and there still aren’t enough rentals being built to meet demand from new households being formed by young people entering the job market or moving away from their parents.

Industry association NAREIT estimates that there is enough pent-up demand to fill roughly 3 million units, which is more than the development pipeline.

“People are living with parents, living with roommates,” said Calvin Schnure, NAREIT’s vice president for research. “It’s uncomfortable.”