A recent report from the National Association of Realtors titled “Expectations & Market Realities In Real Estate 2016: Navigating Through The Crosscurrents” is offering more good news regarding apartment real estate following the positive macroeconomic environment of 2015. What follows is an excerpt from the report:

“Commercial real estate benefited from a positive macroeconomic environment in 2015. Fundamentals continued on an upward trend, as demand for

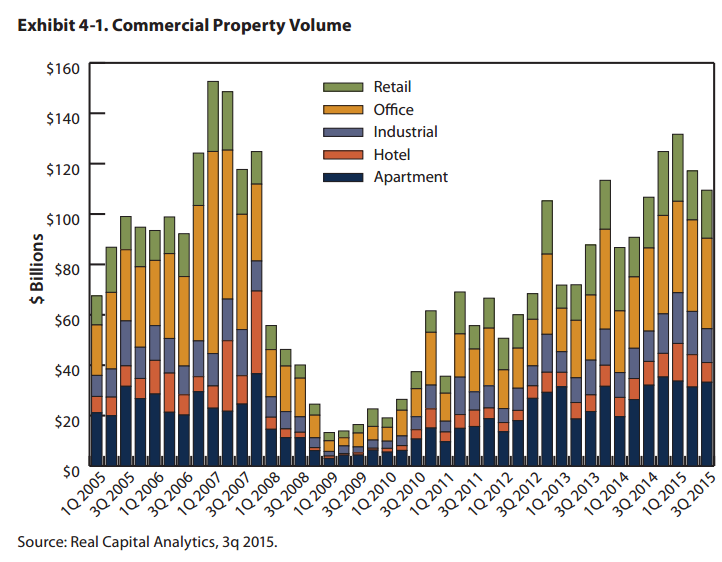

space advanced across all property types, driving vacancies lower and rents higher. With increased capital availability and funding sources, investors pursued deals across the full spectrum of markets seeking yields. The trend led to a higher profile for secondary and tertiary markets, as well as significant gains in prices, which exceeded prior 2007 peaks. Sales of major properties (priced at over $2.5 million) totaled $258.2 billion in the first half of 2015, a 38-percent year-over-year advance, based on data from Real Capital Analytics. Sales volume came close to the $314.1 billion peak reached in the first 6 months of 2007. As shown in Exhibit 4-1, the third quarter 2015 saw an additional $115.3 billion in transactions, bringing the three-quarter total to $375.3 billion.”

The report had much to say about apartment offerings as well, stating that “Apartment assets accounted for 26 percent of all deals, with $98.3 billion in sales.”

Property pricing was also shown to have an optimistic trend leading into 2016. As the following excerpt show, gains since the recession are continuing to grow:

“Commercial property prices rose 16 percent in the first half of 2015 compared with the prior year, according to the Moody’s/Real Capital Analytics  Commercial Property Price Index. Reflecting the rise in transactions, hotel properties posted the strongest price gains by the midpoint of the year, with a 37-percent year-over-year increase. Prices for central business district (CBD) office properties recorded the second-largest gains, with a 24-percent year-over-year increase, moving past their 2007 peaks. Growth in prices for suburban office and apartment properties tied, with an increase of 15 percent each. Industrial prices rose 11 percent from the same period in 2014, while retail properties experienced an 11-percent yearly price appreciation. Prices moved up during the quarter as trends across all of the property sectors held steady in the third quarter of the year (see Exhibit 4-2).”

Commercial Property Price Index. Reflecting the rise in transactions, hotel properties posted the strongest price gains by the midpoint of the year, with a 37-percent year-over-year increase. Prices for central business district (CBD) office properties recorded the second-largest gains, with a 24-percent year-over-year increase, moving past their 2007 peaks. Growth in prices for suburban office and apartment properties tied, with an increase of 15 percent each. Industrial prices rose 11 percent from the same period in 2014, while retail properties experienced an 11-percent yearly price appreciation. Prices moved up during the quarter as trends across all of the property sectors held steady in the third quarter of the year (see Exhibit 4-2).”

The reports as a whole offers an interesting take on upcoming real estate expectations as we step firmly into 2016.

The report was posted on realtor.org and can be found HERE.